The racial wealth gap did not happen by chance. Generations of discriminatory policies and unequal access to financial opportunities have made it harder for many Black communities and people of color to build wealth and achieve long-term financial security. While financial education alone cannot erase these systemic inequities, it is a powerful tool for expanding opportunity. By building credit and providing trusted guidance and personalized support, Prosperity Connection helps people build the skills and confidence to make informed financial decisions and create a stronger financial future.

Explore the historical policies and systemic barriers that have contributed to the racial wealth gap and continue to shape financial opportunities today.

The racial wealth gap is rooted in generations of policies and practices that limited wealth-building opportunities for Black families and other communities of color. One of the biggest contributors is unequal access to homeownership, which has long been the primary way American families build wealth through home equity and passing assets to future generations. As a result, barriers to homeownership have created lasting disparities in financial security and economic opportunity that continue to affect families today.

In their 2021 “Foundations of a New Wealth Agenda” report, the Aspen Institute reported, “Racial disparities in access to credit are so severe that, in the lead up to the Great Recession, white families with annual incomes of less than $30,000 were less likely, on average, to get subprime mortgages compared with Black families with incomes of more than $200,000.“⁴

St. Louis has its own painful, devastating history of housing discrimination and displacement.

In 2022, St. Louis REALTORS® publicly acknowledged the organization’s historical role in housing discrimination that limited homeownership opportunities for Black residents and contributed to the racial wealth gap. Along with this acknowledgment, the organization committed to advancing more equitable housing practices and helping address the lasting effects of these past injustices.¹

In their 2025 Housing Report Reimagining St. Louis: Increasing Black Homeownership, the data highlights the persistent racial disparities in access to homeownership:

Mill Creek Valley

“Victims Out of Site,

Out of Mind?”

St. Louis Post-Dispatch headline, April 6, 1979²

“We bought our house in 1949. We finally paid for it in 1958, but we didn’t get a chance to stay in it for more than a year after that. The Land Clearance Authority told us we had to move, because they were going to build something down there and that we could buy back there if we wanted to after they were finished building.”

– Ollie Green, April 6, 1979²

From the early 1900s until its demolition in 1959 under the banner of urban renewal, Mill Creek Valley was a center of Black life in St. Louis—a thriving community of homes, businesses, schools, churches, and cultural institutions. When the vast majority of the neighborhood was razed, thousands of residents were displaced, disrupting businesses, eliminating homeownership opportunities, and preventing many families from building and passing wealth to future generations.²

Many homeowners received compensation that fell far short of what was needed to rebuild their lives elsewhere. For Thomas and Ollie Green, years of investing in and paying off their home ended with a government buyout that did not provide lasting financial security and was even less than what they spent on renovations. Their family was displaced two additional times over the following decades in the name of redevelopment projects. Each time eliminated the generational wealth they were building for their family. Today, Mill Creek Valley remains a powerful example of how discriminatory housing policies and urban displacement contributed to lasting racial and economic inequities.²

The racial wealth gap is the result of systemic inequities that require many solutions. While financial education and coaching alone cannot eliminate these disparities, they are an evidence-based part of a broader effort to expand economic opportunity. In fact, the Aspen Institute states that households must first be financially stable in order to successfully build sustainable wealth,⁴ which positions the work that we do as an essential initial step. Additionally, the previously mentioned St. Louis Realtors 2025 Housing Report identifies enhancing credit counseling and financial literacy programs as a key strategy for promoting equitable homeownership in our region.¹ At Prosperity Connection, we equip individuals and families with the confidence, knowledge, skills, and personalized support they need to strengthen their long-term financial well-being.

At Prosperity Connection, 67.4% of our clients identify as Black or African American, and 75.7% identify as people of color. By expanding access to free financial education and one-on-one coaching, we help the communities most affected by the racial wealth gap pursue greater financial opportunity and long-term wealth.

Building credit is about access, opening doors to opportunities that support long-term financial stability and wealth building. A strong credit history can help you qualify for affordable loans, secure lower interest rates, and pursue goals like homeownership. While many everyday bills aren’t reported to the credit bureaus, responsibly managing credit accounts, such as credit cards or installment loans, helps build positive credit history. Through financial education and one-on-one coaching, Prosperity Connection helps clients build healthy credit habits that expand financial opportunity and contribute to broader efforts to reduce the racial wealth gap.

A good credit score can open doors to opportunities that support long-term financial stability and wealth building, helping people keep more of their money. Here’s how good credit expands financial opportunity:

Good credit can help you qualify for lower interest rates on loans and credit cards, reducing the amount you pay over time. Utility companies may also waive security deposits for customers with strong credit, allowing you to keep more money in your pocket.

Many landlords review credit reports during the rental application process. A positive credit history can make it easier to qualify for housing and may reduce the amount of your security deposit. Good credit is also an important factor when applying for a mortgage, making homeownership, and the opportunity to build equity, more accessible.

In many states, insurance companies use credit-based insurance scores when determining premiums. A stronger credit history may help lower the cost of auto or homeowner’s insurance.

Good personal credit can make it easier to qualify for business financing, giving entrepreneurs greater access to the capital they need to launch or expand a business.

Some employers, particularly for positions involving financial responsibilities, may review a credit report as part of the hiring process. Maintaining good credit can help remove barriers during a job search.

Good credit can expand access to affordable financial products and reduce the need to rely on high-cost alternatives like payday loans, title loans, or other predatory lending products. By qualifying for healthier financial options with lower fees and interest rates, you can keep more of your money and build a stronger financial foundation.

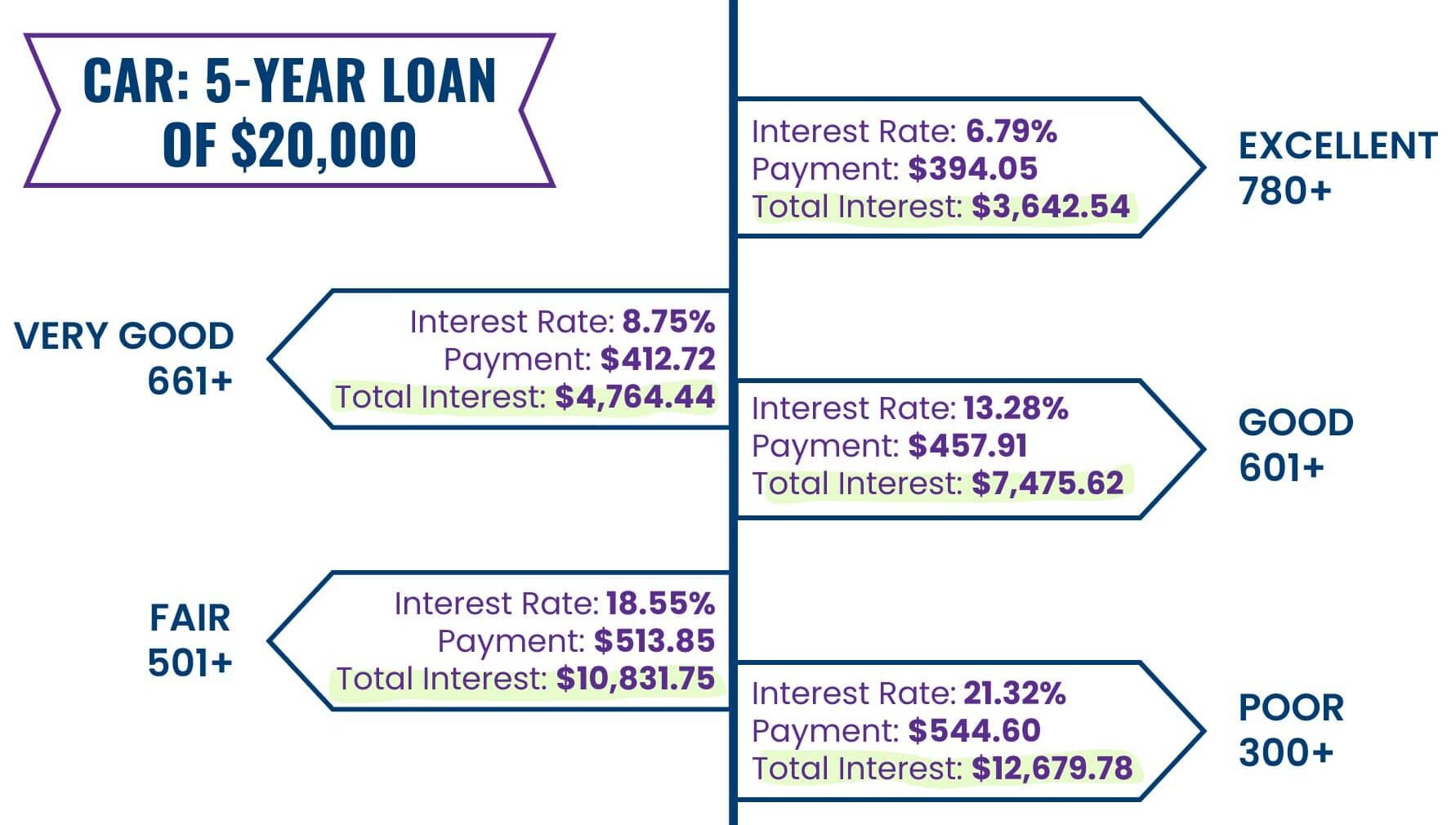

The better your credit, the less you pay to borrow money, leaving more of your income available to save, invest, and build long-term wealth. This example shows how your credit score can significantly affect the total cost of a $20,000 auto loan over five years. A lower credit score could cost you an additional $9,037.24 because of interest.

The data paints a picture of the success for our clients. From 2020 through 2025:

Points was the average increase in credit score

Clients increased their credit score

Credit builder products were opened

Clients went from a subprime credit score to a prime credit score

Of clients felt like they know how to build their credit after their credit report review

Clients established credit for the first time

Building wealth often begins with owning assets that grow in value over time. For many families, homeownership is the first major asset they acquire and one of the most effective ways to build equity. A car may depreciate financially, but it can generate economic opportunity by increasing access to employment, education, healthcare, childcare, and other necessities. That value is tremendous, especially in a car-dependent region like St. Louis.

As wealth grows, families are better positioned to invest in additional assets such as retirement accounts, businesses, and investments. These assets can further strengthen financial stability and create generational wealth.⁴ By expanding access to opportunities like homeownership, we can help more families begin building the assets that reduce the racial wealth gap over time.

For many Black families and other communities of color, a long history of discrimination by financial institutions has created understandable mistrust of the financial system. Additionally, people repeatedly express that accessing financial services can be frustrating, confusing, and overwhelming.³ Prosperity Connection serves as a trusted partner, helping clients navigate that system with confidence.

Financial education drives access to traditional financial services and positively improves trust in banks.³ We connect clients to reliable financial products and services that are truly in their best interest, always providing at least three researched options for clients to choose. The fine print, misleading ads, and predatory practices can be hard to decipher. Our coaches are a trusted, reliable resource clients can count on. We will advocate on their behalf and ensure that they are taken seriously by financial institutions.

Just as importantly, our coaches build lasting relationships grounded in understanding and respect. They recognize that financial decisions are often shaped by personal, family, and community values and responsibilities. That’s why our coaches will help clients create realistic budgets, navigate difficult money conversations, and develop plans that reflect their values and goals.

Tara Price’s journey to homeownership is a great testament to the power of financial education and financial coaching.

Tara dreamed of purchasing a home but wasn’t sure how to make it happen. Although she had steady income, much of it was going toward nightly hotel stays. When she was denied a mortgage, she turned to Prosperity Connection for support. Tara worked with her coach, Veronica, to build a budget, manage her money more intentionally, and pay down collections. With dedication and consistency, Tara raised her credit score by 105 points, which was enough to qualify for a mortgage. Nearly a year after starting her financial coaching journey, she achieved her goal: she purchased a duplex, now living on one side and renting out the other. Tara’s story is a testament to what’s possible with guidance, perseverance, and a clear plan. Her transformation from financial instability to successful homeownership is an inspiring reminder of the power of coaching and self-belief.

Reducing the racial wealth gap takes all of us. Your support helps more individuals and families access free financial education, personalized coaching, and trusted guidance. That can open the door to lasting financial opportunity. Whether you choose to donate or volunteer, you can help create a more equitable financial future in our community.

Sources

1) “Reimagining St. Louis: Increasing Black Homeownership” from St. Louis REALTORS®

2) “Mill Creek: Black Metropolis” from Missouri History Museum

3) “Access to Credit and Financial Services: A Bridge to Financial Well-being” from Federal Reserve Bank of St. Louis

4) “Foundations of a New Wealth Agenda: A Research Primer on Wealth Building for All” from the Aspen Institute Financial Security Program

Akeem Smith (He/Him)

Akeem Smith (He/Him) Mindy Pluma (She/Her)

Mindy Pluma (She/Her) Otis McClure (He/Him)

Otis McClure (He/Him) Genise Lay (She/Her)

Genise Lay (She/Her) Jeff Lash (He/Him)

Jeff Lash (He/Him)

Regina Fowler (She/Her)

Regina Fowler (She/Her) Aaron Tucker Jr. (He/Him)

Aaron Tucker Jr. (He/Him) Nikol Theberge (She/Her)

Nikol Theberge (She/Her) Anniece Robinson

Anniece Robinson  Elizabeth ‘Liz’ Myers (She/Her)

Elizabeth ‘Liz’ Myers (She/Her) Joyce Kampwerth (She/Her)

Joyce Kampwerth (She/Her) Allison Cook (She/Her)

Allison Cook (She/Her) YaNan Bledsoe (She/Her)

YaNan Bledsoe (She/Her)